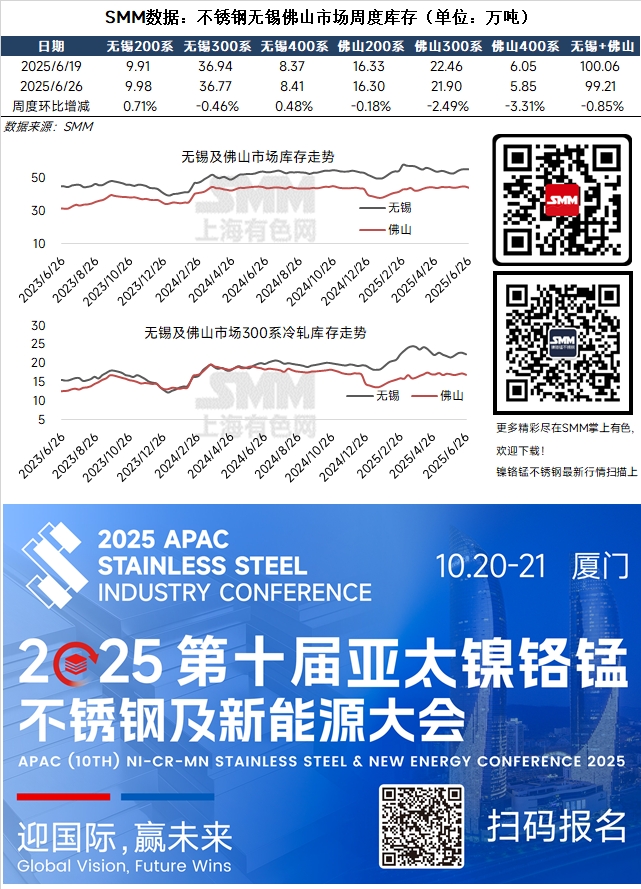

SMM reported on June 26 that during this week (June 20-26, 2025), the total inventory in the two major stainless steel markets of Wuxi and Foshan continued to show a trend of inventory buildup, increasing from 1.0006 million mt on June 19, 2025, to 992,100 mt on June 26, down 0.85% WoW.

At the beginning of this week, stainless steel transactions continued to exhibit a weak trend, with prices falling to a new low in nearly five years. Subsequently, stimulated by news of production cuts at stainless steel mills, stainless steel prices showed signs of stopping falling and rebounding. Although downstream market acceptance of high prices remained limited due to cautious sentiment, transactions of low-priced goods in the market had significantly recovered. After the oversold rebound in stainless steel prices, the enthusiasm of agents and traders for purchasing goods significantly increased, and the situation of futures order-taking also improved notably, alleviating the pressure on in-plant inventory and front-end warehouses of stainless steel mills. Data showed that social inventory of stainless steel had stopped rising and turned to fall, dropping below 1 million mt. However, the downstream demand in the current stainless steel market remained relatively weak. Although transactions improved somewhat during the week due to news of production cuts at steel mills and the oversold rebound in stainless steel prices, the supply-demand imbalance in the market had not yet been truly repaired. Social inventory of stainless steel remained at a relatively high level, and a full market recovery would still take some time.

200-series: Wuxi's 200-series inventory increased from 99,100 mt to 99,800 mt, up 0.71%; Foshan's 200-series inventory decreased from 163,300 mt to 163,000 mt, down 0.18%. 300-series: Wuxi's 300-series inventory decreased from 369,400 mt to 367,700 mt, down 0.46%; Foshan's 300-series inventory increased from 224,600 mt to 219,000 mt, down 2.49%. 400-series: Wuxi's 400-series inventory increased from 83,700 mt to 84,100 mt, up 0.48%; Foshan's 400-series inventory decreased from 60,500 mt to 58,500 mt, down 3.31%.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)